How Insurance works for Rental Car in the USA?

Synopsis

- What Is Rental Car Insurance?

- How do insurance coverages work for rental cars?

- What does a standard car rental insurance policy include?

- Types of rental car insurance

- How rental car insurance works in the USA for US residents?

- How rental car insurance works in the USA for non-US residents?

- Should you buy Extra Rental Car Insurance?

- What are the other alternatives to rental car insurance?

Are you ready to travel? Looking out for hire car insurance? Instead of spending too much time on packing for the trip, review your personal car insurance policy for your own vehicle. What Is Rental Car Insurance?

Rental car insurance covers you against the damages, when you rent a vehicle from a rental car company. Rental car insurance coverage includes vehicle damage, theft, the injuries you cause to third party, your own injuries, and loss of personal items. The rental car company will ask you if you need to add insurance to your car rental or waive the insurance.

How do insurance coverages work for rental cars?

The rental car insurance has three basic types of cover to be on the road - damage cover, theft cover and third-party cover. Here are the Key Things to Know About the Rental Car Insurance. Let’s learn about What does a standard car rental insurance policy include?

Types of Car Rental Insurance:

- Collision Damage Waiver (CDW)– When renting out a car, Collision Damage Waiver (CDW) it includes rental agreement. Collision Damage Waiver (CDW) protects you, if there’s a damage in the car’s bodywork .

-You will end up paying the ‘collision deductible’ at the max - An amount you pay out of pocket to repair or replace the vehicle. Your insurance company covers the rest of the coverage costs as you the claim your car insurance.

Note: This type of cover is a WAIVER and not an insurance. It’s a waiver, where the company waives its right to make you pay the amount for damage.

Which parts of a hire car does Collision Damage Waiver cover?

CDW covers the car's bodyworks, the painted parts – the bonnet, doors, back, wing mirror housings, and side panels.

Which parts of the hire car Collision Damage Waiver does not cover?

CDW does not cover these parts of a rental car - Glass (all windows, lights and mirrors), Tyres & wheels, Flat battery, Interior trim (seats, carpet, and all interior materials), Undercarriage, Gears/transmission, lost keys and personal belongings (includes the boot and glove box).

Should I buy additional insurance coverage when renting a car?

Yes, as there are limitations under Collision Damage Waiver (CDW), it is better to buy additional insurance coverage.

- What are the damages collision damage waiver does not cover?

You are liable for the entire amount in the circumstances provided below.

- When the rental car's bodywork gets damaged due to illegal parking

- When the parts of the hire car not covered by Collision Damage Waiver gets damaged

- Speeding or drink-driving

- When you damage the third-party vehicles or their property or if there are bodily injuries

- In case of a traffic accident due to your fault

- Theft-Protection – If the hire car is stolen, Theft Protection covers the cost for replacing the hire car. The covers includes repair costs for the damage caused, when someone tries to steal it.

- If you violate your rental agreement, for example, if you had left the car unlocked, you are liable for the entire cost of replacing the rental car. - Personal Effects Coverage

Personal Effects Coverage covers the loss or theft of personal items.

-If someone steals your clothing and luggage from the rental vehicle,

-If you lose the personal items, when someone steals the rental vehicle

Note: Expensive electronics such as cameras and smartphones may be subject to limits and exclusions.

Average cost: $1–6 per day

Comparable to: Homeowner’s and renter’s insurance

Should I buy Personal Effects Coverage (PEC) when renting a car?

If you have a renters or condo policy, homeowner’s policy, it will cover your personal items if someone steals them from a rental car. Check your policy documents to ensure you elect or decline this coverage.

- Personal Accident Insurance

Key things to know about the Personal Accident Insurance:

Personal Accident insurance covers minor damages and major disabling incidents due to an accident - injuries that include a broken limb, loss of a limb, burns, lacerations, or paralysis.

Personal Accident insurance also includes services which the health insurance does not cover - copayment, deductible, physiotherapy, and any out-of-pocket expense from the accident.

- In case of your accidental death, accident insurance pays out money to your designated beneficiary.

Why is Accident insurance deemed supplemental insurance?

Accident insurance covers non-medical costs like utility bills, mortgage or rent, and other daily expenses.

Payouts come in cash immediately with the accident insurance.

What does personal accident insurance not cover?

- Only after you activate the policy and pay your first premium policies pay for your injuries.

- Personal accident insurance does not cover self-inflicted injuries.

- Injuries caused by illegal or criminal activities are not covered by accident insurance.

- If the injuries are caused by extreme sports such as bungee jumping or scuba diving, accident insurance don't cover them.

- If you have been driving under the influence of alcohol or drugs, accident insurance will not cover your injuries.

- If you get into the accident due to illnesses such as seizures or heart failures, accident insurance will not cover the injuries.

- Rental Car Liability Insurance

Key things to know about the Liability insurance

Liability insurance covers only the damage you cause to other vehicles, people, and properties when you drive your rental car.

What the Liability insurance do not cover?

-You, the rental vehicle, or your passengers.

Note: Additional insurance purchases will provide higher coverage limits.

-The state minimum levels of liability insurance are a part of the basic rental fee in almost every state.

Exception: In California, the law does not require the rental companies to include liability insurance.

Average cost: $10–16 per day

Comparable to: Bodily injury liability and property damage liability insurance

How rental car insurance works in the USA for US residents?

What are the sources that provide insurance coverage for rental cars?

For all US-residents

- Personal car insurance

- Health insurance,

- Credit card benefits

- Existing travel insurance

How rental car insurance works in the USA for non-US residents?

For non-residents

- You need to apply for an International driving permit (IDP) with the department of motor vehicles in your country. With an international driving license, you can drive in many countries including the United States.

- Then purchase a travel insurance policy and additional insurance to ensure you are only liable pay an excess amount.

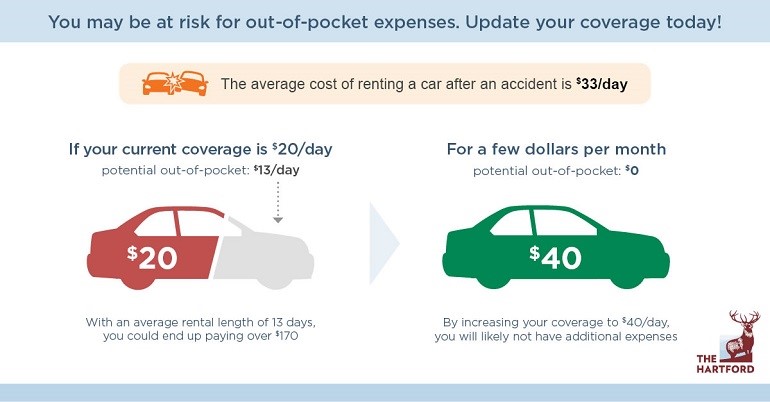

Should you buy Extra Rental Car Insurance?

Watch for the gaps in personal coverage - Some policies have exclusions that will leave you with gaps in the coverage.

Potential Auto Insurance Gaps

- The auto insurance policy does not cover collision

- Your collision coverage does not include rental vehicles

- Some auto insurance policies only cover certain rental vehicles

- Your policy excluded the Loss of use and diminution of value coverage

Potential Credit/Debit Card Gaps

- If you split the cost between two cards, it will void the coverage

- If you fail to activate the coverage

- If you are using debit card instead of a credit card (Debit cards don't come with benefits)

- If you exceed the maximum days of coverage

What are the other alternatives to rental car insurance?

- Non-owner car insurance

- Temporary car insurance

- Travel insurance

Info source: Wallethub.com, vroomvroomvroom.com

Planning a trip? Plan ahead and compare taxi rates. You can save money and time with car rides rather than spending money on rental cars. With Elife Transfer, you can travel between cities stress-free with our shared rides - Sedan, Minibus, Minivan, or SUV. Rent a car at All-Inclusive-Rates including taxes, tips, and tolls, all confirmed before booking. Now avail: Instant ride fares, All-Inclusive-Rates, a 60-minute waiting period and a full refund by cancelling your service up to 24 hours prior.

Download Elife App now!